How to start an accounting firm in the UK: a comprehensive guide

Run your entire firm on one platform

Starting an accounting firm in the UK in 2026 means navigating a market that has changed significantly in recent years. Making Tax Digital for Income Tax Self Assessment is now live, AML supervision requirements have tightened, and firms are consolidating their tech stacks to stay competitive with larger practices.

But the opportunity is real. Demand for qualified accountants continues to outpace supply, and cloud technology has lowered the barrier to entry for running a modern, remote-first practice. Many successful UK firms today were launched by solo practitioners working from home with a laptop and the right software.

This guide walks through the professional, legal, and operational steps to launching your own accounting firm in the UK including the costs, timelines, and compliance obligations most guides skip. Let’s start with why it’s worth doing in the first place.

Table of сontents

- Why start an accounting firm in the UK?

- Key steps involved in starting an accounting firm in the UK

- Obtaining the qualifications required for an accountant

- Applying for a practising certificate

- Registering for AML supervision

- Creating a business plan

- Choosing a business structure

- Submitting a notification of incorporation

- Getting the right insurance

- Marketing your business

- What is the best accounting software for accounting firms?

- Frequently asked questions

- To sum up

Table of сontents

- Why start an accounting firm in the UK?

- Key steps involved in starting an accounting firm in the UK

- Obtaining the qualifications required for an accountant

- Applying for a practising certificate

- Registering for AML supervision

- Creating a business plan

- Choosing a business structure

- Submitting a notification of incorporation

- Getting the right insurance

- Marketing your business

- What is the best accounting software for accounting firms?

- Frequently asked questions

- To sum up

Why start an accounting firm in the UK?

While this article focuses mainly on how to start an accounting firm in the UK, it’s also important to touch on why. There are plenty of compelling reasons why you might want to launch your own accounting firm, both personal and professional. In this section, we’ll highlight some of the most important things to consider.

1. The accounting talent shortage

In recent years, there has been a growing talent shortage in the UK accounting industry. This has been fuelled by a combination of factors, including the retirement of baby boomer accountants, changing educational trends, and the threat of automation. This means that accounting skills are in high demand, and accounting firms can charge more to meet client needs. In recent years, salaries for finance professionals have consistently outpaced the UK national average, giving qualified accountants strong leverage whether they stay employed or set out on their own.

2. Growing demand for accounting services

In addition to the talent shortage, demand for accounting services is being fuelled by an increasing number of small-to-medium-sized businesses (SMEs) in the UK. Despite a slight downturn during the COVID-19 pandemic, the number of SMEs has been growing steadily over the last decade or more as digital technologies lower barriers to entry and open new professional frontiers.

3. Uncapped growth potential

As a business owner, you get to set the rates, decide how many clients you can take on and what hours you want to work. In other words, the only restrictions to growth and earnings are the ones you impose on yourself. This is in stark contrast to a typical salaried position, where earnings and professional growth are somewhat limited by factors you cannot directly control.

4. Professional freedom

Besides uncapped earning potential, becoming a business owner provides complete professional freedom. You get to decide the services you’ll offer, the clients you’ll help, how your business will be marketed, the pricing structure — everything. This adds an extra dimension to your professional life. In addition to being an accountant and helping clients manage their finances, you are also the captain of your own ship, making work more intrinsically rewarding.

Key steps involved in starting an accounting firm in the UK

Now that we’ve discussed the why, let’s get down to the nitty-gritty: how exactly do you go about starting an accounting business in the UK? Below, we’ll run through some of the key steps and considerations.

- Obtaining the qualifications required for an accountant

- Applying for a practising certificate

- Creating a business plan

- Choosing a business structure

- Submitting a notification of incorporation

- Getting the right insurance

- Marketing your business

- Choosing the right software

Obtaining the qualifications required for an accountant

To start an accounting firm in the UK, you need to have the prerequisite experience and qualifications.. Many start with a bachelor’s degree in accounting, finance, or another related field, while others study for the AAT (Association of Accounting Technicians) qualification. These professionals may then study to become chartered accountants.

Either way, you’ll need relevant qualifications and work experience to be taken seriously as an accounting professional. To start your own firm, the more experience you have, the better service you’ll be able to provide to your clients. Depending on the qualification you go for, you’ll need to become a member of one of the UK’s professional accounting bodies, which include:

- Association of Accounting Technicians (AAT)

- Association of Chartered Certified Accountants (ACCA)

- Chartered Accountants Ireland (CAI)

- Chartered Institute of Management Accountants (CIMA)

- Chartered Institute of Public Finance and Accountancy (CIPFA)

- Institute of Chartered Accountants in England and Wales (ICAEW)

- Institute of Chartered Accountants of Scotland (ICAS)

Applying for a practising certificate

To set up a public practice in the UK, you’ll also need to hold a practising certificate (PC). This involves an application process with your professional accounting body. Practising without a PC can result in disciplinary action, so this is a crucial step to take.

While each professional body has its own rules and requirements for issuing PCs, you generally need to demonstrate that you have the prerequisite skills, experience, and qualifications in the areas you intend to practise, including being up to date with professional ethics qualifications and continuous professional development (CPD).

Registering for AML supervision

All accountants and bookkeepers providing services in the UK must be supervised for Anti-Money Laundering (AML) compliance under the Money Laundering Regulations 2017. This is a legal requirement, not an optional step.

If you are supervised by a professional body such as ACCA, ICAEW, CIMA, or AAT, that body typically acts as your AML supervisor. You should confirm your status directly with them, as requirements and arrangements may vary.

If you are not supervised by a professional body for example, if you operate independently, you must register with HMRC for AML supervision before starting to provide regulated services. Failing to do so can result in significant penalties, including criminal sanctions.

Your ongoing AML obligations will include:

- Carrying out client due diligence (ID verification) before onboarding any new client

- Maintaining a written firm-wide risk assessment

- Appointing a Money Laundering Reporting Officer (MLRO), which in small practices is usually the firm owner

- Keeping records of client due diligence and transactions for a minimum of five years

- Filing Suspicious Activity Reports (SARs) with the National Crime Agency when required

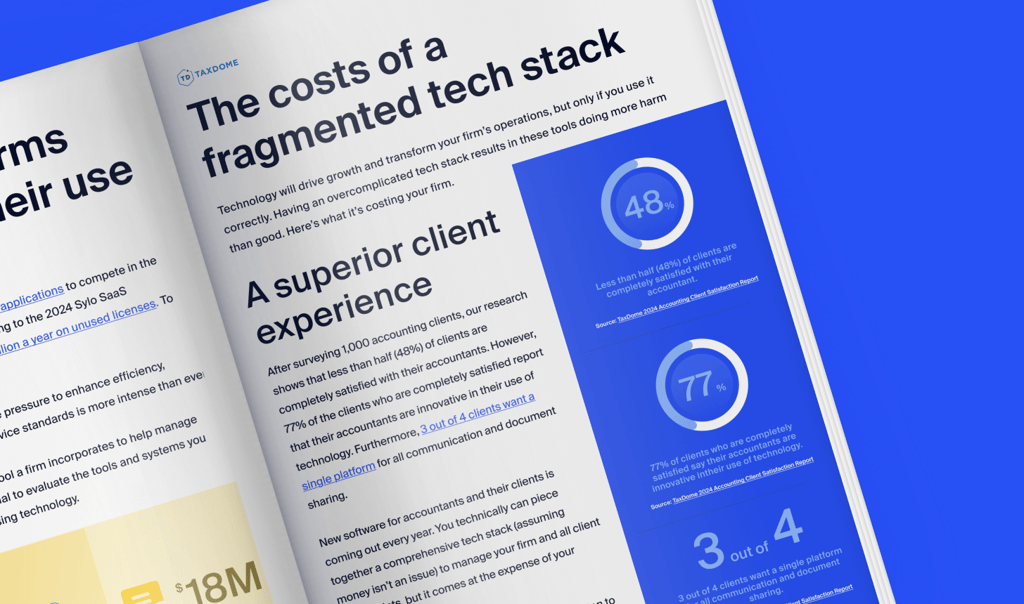

The administrative burden of AML compliance is one reason many UK firms adopt practice management software to centralize client onboarding, automate ID verification, and securely manage documents reducing time spent on compliance and manual client follow-ups.

Creating a business plan

Before you get up and running, it’s important to spend some time creating a comprehensive business plan. This will help guide you on your journey, ensuring that you stay focused and on track. Here are some questions to ask to help you with this process:

Company basics:

- What will your company be called? You can check the Companies House register to see whether your preferred name is available.

- Where will it be located?

- Will you rent office space or work from home?

Financing your business:

- How much money do you need to get the company off the ground?

- Will you need to secure loans, credit, or investment?

- What are your financial forecasts and targets?

Services and pricing:

- What kind of clients would you like to serve? (E.g. individuals, small businesses, etc.)

- Do you want to offer general accounting services or more specialist offerings?

- How will your services be priced?

Market research:

- What services do direct competitors offer?

- What marketing strategies do they implement?

- What are competitors doing well and what could they do better?

Choosing a business structure

Choosing the right business structure is a crucial decision that will impact your legal obligations, tax liabilities, and the overall complexity and cost of running your business. Let’s look at the options.

Sole trader business

A sole trader, also known as a sole proprietorship, is the simplest business structure to set up and run. As a sole trader, you have complete control over your business decisions, but from a legal perspective, there’s no separation between you (the owner) and the business. That means you are liable for any debts incurred or other legal obligations. From a tax perspective, any profit you enjoy will be taxed at your regular personal income tax rate.

Pros:

- Relatively simple to set up

- Complete control over how the business is run

- Simple accounting and tax filings

Cons:

- You are liable for business debts

- Limited opportunities for securing loans or investment

- Could be seen as less professional compared to a limited company

Partnership

Another option is a partnership, where you go into business with one or more trusted partners. Depending on the type of partnership you set up, you share responsibility for the business, including any losses or legal obligations. Profit is also shared between partners, with each partner paying individual income tax on their share.

There are three different types of partnerships in the UK:

- General partnership: all partners share liability and decision-making equally

- Limited partnership (LP): includes both general and limited partners, the latter of which contribute capital and share in any profits but have limited liability and do not participate in the management of the business

- Limited liability partnership (LLP): offers the benefits of a partnership with limited liability protection, meaning partners are not personally liable for the debts of the business

Pros:

- Shared responsibility and resources

- Simple and cost-effective to set up

- Partners bring diverse skills, experience, and expertise

Cons:

- Partners are jointly and severally liable for business debts

- Having multiple business owners increases the risk of disputes

- You don’t have full control over business decisions

Limited company

Unlike sole trader businesses and general partnerships, a limited company forms a separate legal entity from its owner(s). That means the business is responsible for any debts, not the owner(s). In most cases, limited companies are owned by shareholders, but they are run by directors.

There are two main types of limited company:

- Private limited company (Ltd): this type of business is not publicly listed, meaning shares cannot be sold to the general public. This structure is often used by small to medium-sized businesses.

- Public Limited Company (PLC): this type of business is listed on a stock exchange, meaning the general public can buy shares and own equity in the business. PLCs are typically larger businesses.

Pros:

- Limited liability for shareholders

- Potentially more tax-efficient, with various options for salary and dividend distributions

- Limited companies may provide more credibility to clients and investors

Cons:

- More complex and costly to set up and maintain

- More stringent administrative responsibilities, including filing annual accounts and confirmation statements

- Directors have legal responsibilities and duties

Submitting a notification of incorporation

If you choose to set up a limited company (Ltd, PLC), a limited liability partnership (LLP), or any other business structure where your business is incorporated (i.e. it becomes its own legal entity), you’ll need to submit a notification of incorporation to your professional accounting body.

These forms generally include basic information about the firm, its partners, shareholders, professional indemnity insurance, and the services it offers. You’ll also need to notify your professional accounting body about any key changes to your business.

Getting the right insurance

As an accounting business, you’ll be working with sensitive financial and personal information, as well as advising clients on critical accounting matters. To protect your business from potential risks and liabilities, it’s important to have the right insurance coverage. Here are some examples to be aware of:

- Professional indemnity insurance: this provides you with coverage against claims made by clients against you for advice or actions that supposedly caused them financial loss or damage. This type of insurance is generally a legal requirement for membership in professional accounting bodies.

- Employer’s liability insurance: this is a legal requirement if you plan to hire employees, providing coverage against any claims made by employees who suffer work-related injuries or illnesses

- Cybersecurity insurance: this protects you against any cyberattacks or data breaches you may suffer that compromise sensitive client information. While not a legal requirement, this type of coverage is increasingly important in a digital-first world.

- Business interruption insurance: this provides coverage against operating expenses and any loss of business income as a result of an unforeseen event, such as a fire, flood, or other natural disaster.

- Business content insurance: this covers you against the loss, damage, or theft of the physical assets of your business, including office equipment, furniture, and supplies.

Marketing your business

Now, it’s time to tell the world that your business exists! There are countless ways you can do this, but in a digital-first world, the following form a solid foundation for attracting new clients:

- A well-structured and professional business website

- SEO-optimised website content to generate organic traffic

- Content marketing, including regular blog posts, video content, or case studies

- Social media marketing to engage the community and build brand awareness

- Email marketing to generate leads and acquire new clients

What is the best accounting software for accounting firms?

One of the biggest decisions you’ll make as an accounting firm owner is which software to use. Why? Because accountants rely on software to streamline and automate virtually all of their tasks and workflows. The tech you choose will have a direct impact on how efficient your firm is, how much money you make, and how satisfied your clients are.

So, what is the best software for accounting firms? While there are countless tools and apps you can use to make accounting processes smoother, there are two essential parts of an accounting tech stack: accounting software and practice management software. Let’s look at these in more detail.

Accounting software

Accounting software provides all the tools you need to manage your day-to-day accounting work, from account reconciliations to expense tracking, financial reporting, and much more. Examples include QuickBooks Online, Xero, or Sage Intacct.

Practice management software

With accounting software handling the actual accounting work, practice management software handles everything else you need to run a highly efficient and profitable accounting business. Take TaxDome, for example, which combines powerful tools for managing your clients, teams, projects, documents, and workflows, all in one place.

For a deeper dive into TaxDome’s core functionality and how it can transform your accounting practice, check out this overview video:

Frequently asked questions

Do you need to be a chartered accountant to start an accounting firm in the UK?

No, you don’t need to be a chartered accountant. You can start an accounting or bookkeeping business without formal qualifications, but you must be competent and registered for AML supervision.

If you are a member of a professional body (such as ACCA, ICAEW, AAT, etc.), you will usually need a practising certificate to offer services to the public.

How long does it take to start an accounting firm in the UK?

Many practitioners can launch within a few weeks to a few months once their qualifications and practising certificate are in place. Key steps such as AML registration, business incorporation, and software setup typically run in parallel and take 2 to 4 weeks.

Can I start an accounting firm from home in the UK?

Yes, and many successful UK firms operate entirely from home. You’ll need to comply with ICO data protection requirements and GDPR, check any restrictions in your residential tenancy or mortgage agreement and ensure your setup meets any requirements set by your professional body, if applicable.. A cloud-based practice management platform makes a fully remote setup straightforward and ensure your setup meets any requirements set by your professional body, if applicable.

What’s the difference between a bookkeeper and an accountant in the UK?

Bookkeepers generally handle day-to-day transaction recording, bank reconciliations, and VAT returns, and can operate under AAT licensing or direct HMRC AML supervision. Accountants typically handle statutory accounts, tax returns, and advisory work, and usually hold qualifications through ACCA, ICAEW, or a similar body.

Do I need professional indemnity insurance as a UK accountant?

Yes. It is a requirement for practising certificate holders with all major UK professional bodies. Minimum coverage levels vary by body, and most link the minimum cover amount to your gross fee income.

Is Making Tax Digital relevant when starting my firm in 2026?

Yes. Making Tax Digital for Income Tax Self Assessment is is being phased in and will expand as a part of the UK tax landscape.. Any firm launching today should build its software stack around MTD compatibility from day one, both the accounting software used to prepare returns and the practice management software used to coordinate quarterly client workflows.

To sum up

There are plenty of reasons to consider starting your own accounting firm in the UK, from growing demand for accounting services to the freedom to forge your professional path. There are plenty of challenges, too — but with the right planning and preparation, they can easily be overcome.

We hope you’ve found this guide helpful. If you do decide to start your own business, remember that one of the biggest factors in your new firm’s success will be the technology you use. With a comprehensive practice management platform like TaxDome, you can increase efficiency, automate entire workflows, and provide a truly stellar client experience.

But don’t just take our word for it — request a demo and see for yourself!

Nicholas produces TaxDome content focused on how technology improves accounting workflows and everyday firm operations.

Get your free guide

Thank you!

The guide copy has been sent to your email. Please check your inbox!

Recommended articles

Best payroll software for accountants in 2026: features, tools, and what to look for

10 best AI software solutions for accounting in 2025

8 best tax practice management software for accountants and tax professionals in 2026