#Accounting templates, #Accounting workflow

Year-end accounting checklist for 2024: closing the fiscal year

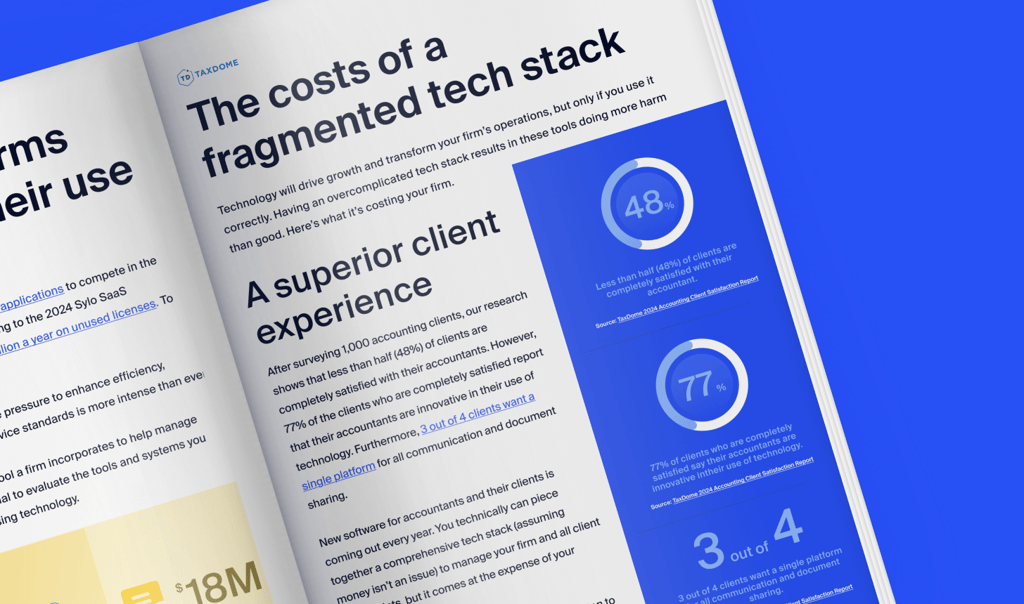

Run your entire firm on one platform

As the calendar pages turn and the end of the fiscal year approaches, it’s time to prepare for your firm’s year-end close.

A successful year-end close requires meticulous planning and execution to ensure the financial health of any business. A comprehensive year-end accounting checklist is one of the most effective tools we’ve found for an accountant’s arsenal during this time.

In this article, we’ll show you how to navigate the complex tasks ahead while maximizing efficiency and minimizing errors.

Table of сontents

What is the year-end close?

The year-end close in accounting is the process of reviewing and finalizing all financial activities within your firm for the fiscal year. This process is crucial for ensuring that your firm’s financial records accurately reflect its operations in accordance with basic accounting principles. By adhering to these principles, the year-end close helps guarantee that financial statements are comprehensive and can withstand the scrutiny of an audit.

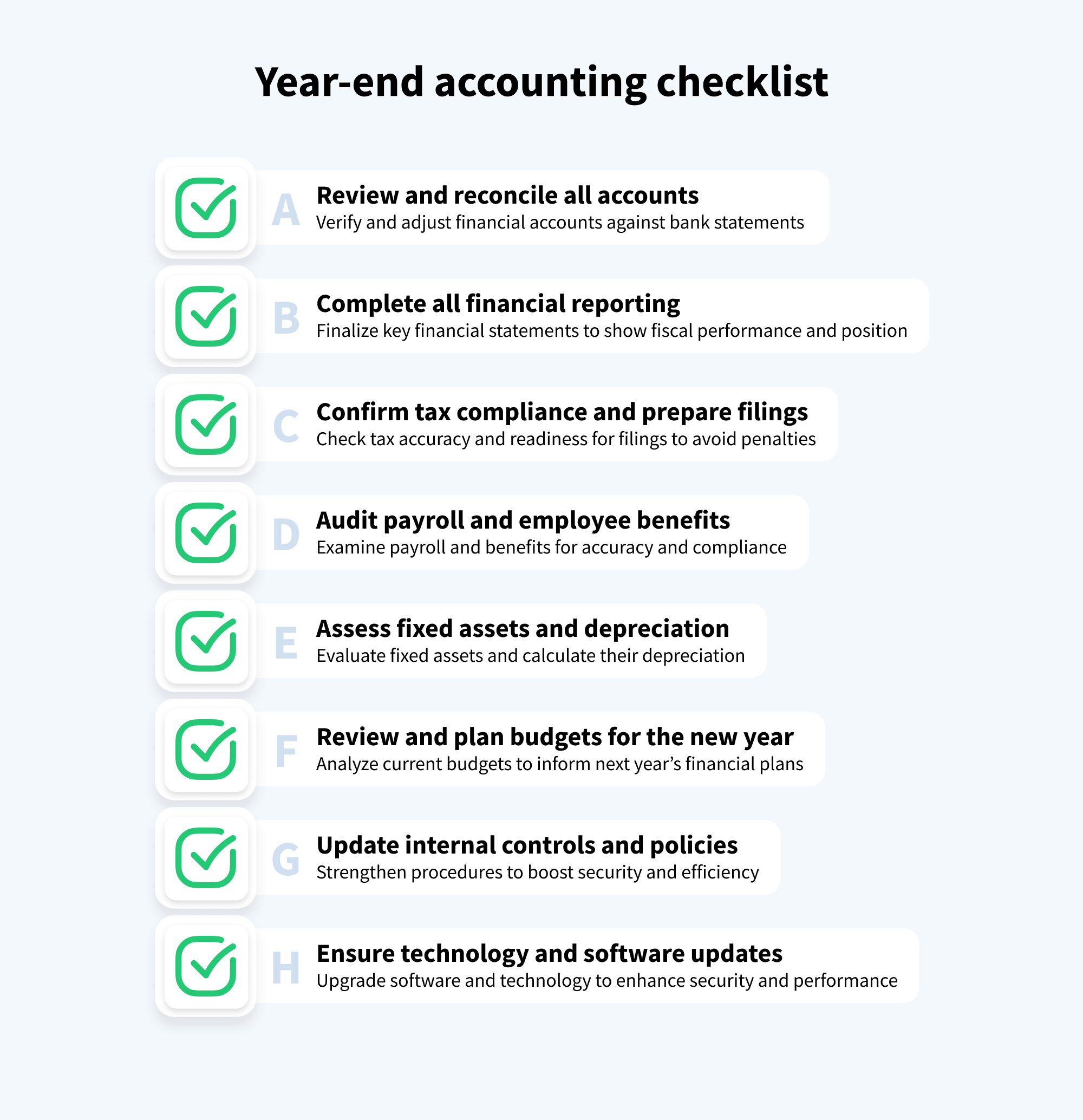

Year-end accounting checklist

To close the fiscal year systematically and save valuable time, let’s explore a checklist we’ve prepared to prevent anything from slipping through the cracks.

Review and reconcile all accounts

Begin the process by reviewing and reconciling all accounts. This includes conducting an accounting true-up to ensure accuracy across all records. Make sure to review the following:

- Cash accounts: verify all cash account balances by reconciling them with bank statements and other financial records.

- Accounts receivable: review all outstanding invoices and compare them with customer payments. Identify any discrepancies or bad debts that need to be written off.

- Fixed assets: assess all fixed assets, including property and equipment. Check for accuracy in recording acquisitions, disposals, and depreciation.

- Accounts payable: verify all records of amounts your firm owes. Ensure that all invoices are accounted for and that payments are current.

- Accrued expenses and other liabilities: review all accrued expenses, such as wages, taxes, and utilities, to confirm that they accurately reflect the amounts owed but still need to be paid.

- Prepaid expenses: check accounts to confirm that expenses paid in advance are correctly allocated. For instance, if the company pays for a year-long insurance policy, ensure that the monthly portions are correctly expensed over the year.

- Equity accounts: if applicable, review changes in equity accounts, including owner’s capital, withdrawals, and retained earnings. This step ensures that all changes, like dividends paid or earnings retained, are correctly reflected in the company’s equity.

Complete all financial reporting

The next step is completing all financial reporting. This includes preparing, reviewing, and finalizing primary financial statements summarizing your firm’s financial performance and position.

First, preparing your balance sheet will provide a snapshot of the firm’s financial position. It should include all assets, liabilities, and equity. Next, your profit and loss statement is necessary to show your firm’s revenues, expenses, and profits over the fiscal year. In addition to these, you’ll also want to complete the following:

- Cash flow statement: compile the cash flow statement, which details the inflows and outflows of cash during the fiscal year. Accurate cash flow reporting is essential for understanding the liquidity and financial flexibility of the business.

- Statement of retained earnings: prepare the statement of retained earnings, which shows how the retained earnings portion of equity has changed during the reporting period. This includes starting retained earnings, net income or loss, dividends paid, and other adjustments. This statement links the income statement and balance sheet and provides insight into how profits are used (reinvested or withdrawn).

Be sure to include any valuable notes and supplementary information, such as accounting policies, details about contingent liabilities, or commitments not reflected directly in the financial statements mentioned above.

Confirm tax compliance and prepare filings

Taking the extra time to double-check you’re compliant when preparing your filings is time well spent, as it safeguards your firm against potential audits or financial penalties.

Start by gathering invoices, receipts, payroll records, and any other necessary documentation that supports accurate tax calculations and helps to avoid an audit. Be sure to carefully review all deductions and credits your firm plans to claim, including standard deductions such as operating expenses, employee benefits, and depreciation, as well as more specific items like green energy incentives or industry-specific credits.

Audit payroll and employee benefits

Fair compensation is an excellent general business practice that helps keep employees motivated throughout the years. Reviewing this during the close of the fiscal year is the perfect time.

Take the time to examine all salary and wage records. Compare current salaries and wages against employment contracts and previous payroll records, and make sure that each employee’s pay is consistent with the market.

For employees earning commissions or bonuses, verify that the amounts paid align with targets and achievements. Additionally, you may need to review overtime payments to be sure they align with your firm’s policy and are legally compliant.

Assess fixed assets and depreciation

Assessing fixed assets and calculating depreciation helps to accurately report the value and usage of your firm’s long-term assets. Keeping this information up-to-date and accurate is vital for evaluating investment returns, strategizing future purchases or disposals, and maintaining compliance with standards. To effectively manage this process, follow these steps:

- Review your fixed asset register: update it to ensure it accurately reflects all current assets, including details like purchase dates, costs, accumulated depreciation, and book value.

- Verify asset purchases and disposals: check for any new purchases or disposals during the year. Accurately record these changes in the fixed asset register and general ledger, including any gains or losses from the sale or disposal of assets.

- Conduct a physical inventory of your assets: verify all listed assets to confirm their existence and evaluate their condition. This process helps identify any discrepancies, such as assets that are lost, no longer usable, or not previously recorded.

- Calculate and record depreciation: use an appropriate depreciation method to calculate depreciation for each asset during the fiscal year. Update the depreciation in the fixed asset register and record the depreciation expense in the income statement.

- Adjust for asset impairment: assess each asset for signs of impairment. If impairment is detected, adjust the asset’s book value on the balance sheet and record it in the income statement.

- Create reports with notes: prepare reports on fixed assets and depreciation. These notes should explain significant changes, policies applied, and any other relevant information to provide stakeholders with a clear picture of your firm’s asset management and depreciation practices.

Review and plan budgets for the new year

With all the information you gather during the year-end close, it’s essential to add planning to your year-end accounting checklist. Start by analyzing the current year’s financial performance against the budget and identifying any variances. Using this information, you can develop detailed revenue and expense forecasts and strategic objectives for the following year.

One way to improve this process is to incorporate practice management software when you close the fiscal year. Advanced practice management software offers data-driven insights with reporting analytics to automatically gather your firm’s data and organize it in a way that will help you effectively plan for your firm’s future.

Update internal controls and policies

By reviewing existing controls, you can identify and strengthen weak or outdated areas in your year-end close process that can improve compliance. After reviewing existing controls and policies during a year-end close, you may find yourself wanting to improve security by:

- Incorporating regulatory updates

- Strengthening the segregation of duties

- Enhancing access controls

- Improving documentation and record-keeping

Additionally, regular staff training on these updated practices helps improve the implementation of any policy changes. Afterward, seeking feedback from your team can help you continue to improve these processes to keep them effective and compliant.

Ensure technology and software updates

Not only is having the most up-to-date technology and software good for security, it also significantly impacts your firm’s efficiency through all sorts of accounting processes. By updating to the latest accounting software, your firm can utilize enhanced features and improve functionality to promote accurate financial reporting.

To determine how your firm can incorporate accounting technology to improve this and other processes, consider following these steps:

- Update your current accounting software: update your software to the latest version to reduce the risk of errors

- Review and assess additional software needs: examine your current tech stack to identify any gaps where additional software could improve efficiency, security, or data management

- Research options: look for additional software solutions that meet any needs not currently met

- Check for integration: verify that any new software you choose integrates with other essential software to streamline data and workflows

- Evaluate and plan for future upgrades: regularly assess your firm’s use of software to keep everything aligned with evolving business needs

Best practices for an efficient year-end close

To enhance the efficiency and accuracy of the year-end close process, you should start by planning and preparing early. Establishing a clear timeline and preparing all necessary documentation well in advance helps prevent last-minute rushes and enables a smoother process.

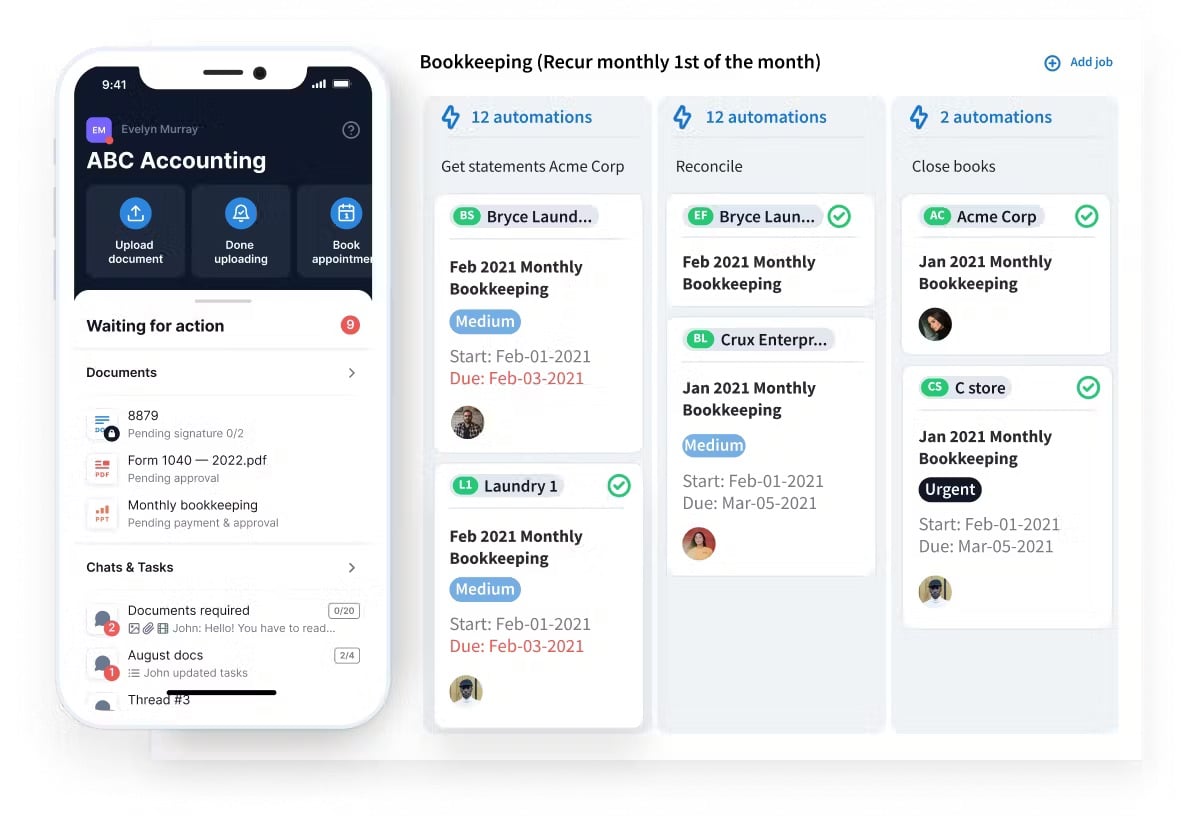

Using practice management software can also help here. By leveraging accounting technology to automate routine tasks such as data entry, calculations, and report generation, you create more available time for your team to focus on high-level tasks, such as the year-end close.

TaxDome is a prime example of this type of practice management software. It helps your staff fully focus on the most important work in your firm by eliminating routine tasks that consume too much of their time. It also offers valuable insights and analytics into how your firm functions so you can identify areas of improvement and get your firm running at full capacity.

Maintaining regular reconciliations throughout the year also helps as it detects and corrects discrepancies early on, so you don’t have a pile of work at the end of the year. Be sure to document effective practices to help continuously improve your processes each year.

Common pitfalls and how to avoid them

It takes time to create a perfect process, and each firm has unique needs during its year-end close. However, to avoid falling prey to common mistakes, here are a few common pitfalls and how to avoid them.

1. Procrastination and poor planning

- Delaying the start of the year-end close process can lead to rushed work, increased errors, and unnecessary stress

- Begin planning well in advance by setting a clear timeline and checklist for all year-end tasks so you have time to address issues without the pressure of looming deadlines

2. Lacking documentation

- Poor record-keeping throughout the year can lead to difficulties in making accurate adjustments

- Maintain thorough and timely documentation of all financial transactions and decisions throughout the year with a consistent documentation policy to ensure all necessary information is recorded and easily accessible

3. Poor reconciliation practices

- Failing to reconcile accounts regularly can result in undetected discrepancies that accumulate and complicate your year-end close

- Establish routine reconciliation processes, such as monthly or quarterly reviews, to identify and correct discrepancies early

4. Reliance on outdated processes

- Using outdated software or methods can slow down processes and increase the risk of errors

- Update your accounting software by investing in new technology that improves efficiency and accuracy

Conclusion

Your accounting year-end close demands total focus and flawless execution. With so much on the line, accounting firms need help to ensure their practice functions at its best. Planning and utilizing technology such as practice management software go a long way in keeping your year-end closed organized and freeing up time so your staff can give their full attention to this vital task.

Jeff writes for TaxDome with experience in accounting, finance, and invoicing industries. He focuses on educating users about accounting trends and maximizing productivity through practical guidance on TaxDome’s features.

Get your free guide

Thank you!

The guide copy has been sent to your email. Please check your inbox!

Recommended articles

ChatGPT for accountants: 12 strategies to automate your workflows

12 best free online accounting courses with certifications for 2026

Top 9 free online bookkeeping courses with certificates in 2026