Buying an accounting practice: your ultimate guide

Run your entire firm on one platform

Key takeaways:

- Buying an accounting practice lets you skip the demanding startup phase and step into an established firm with clients, staff, revenue, and reputation.

- The right fit starts with getting specific: define goals, ideal firm size, services, niche, and location before looking at listings.

- Thorough due diligence is a must. Look at financial health, client base, staff expertise, work culture, and tech stack before agreeing a deal.

- Cash flow, client retention, and resistance to change are big post-acquisition risks, so go in with a decent financial buffer and overcommunicate with both clients and staff.

- A strong practice management platform can help the transition by giving your new firm structure, improved efficiency, and a better client experience.

There are many paths to success in the accounting industry. Some accountants climb the ranks of the corporate ladder, going on to become financial controllers, accounting directors, or even CFOs. Others take their experience and start their own accounting businesses from scratch.

One route is often overlooked, however: buying an accounting practice.

In this article, we’ll explain everything you need to know about buying an accounting business — from the key benefits and challenges to practical tips and advice on how to find the best deals.

To provide firsthand insights into the process, we also teamed up with Andrea MacDonald, CPA, a firm owner who’s built her business through strategic acquisitions. Over the past decade, Andrea has grown Steadfast Bookkeeping by merging multiple practices into one and has learned a lot along the way.

But before we jump in, let’s answer a crucial question.

Table of сontents

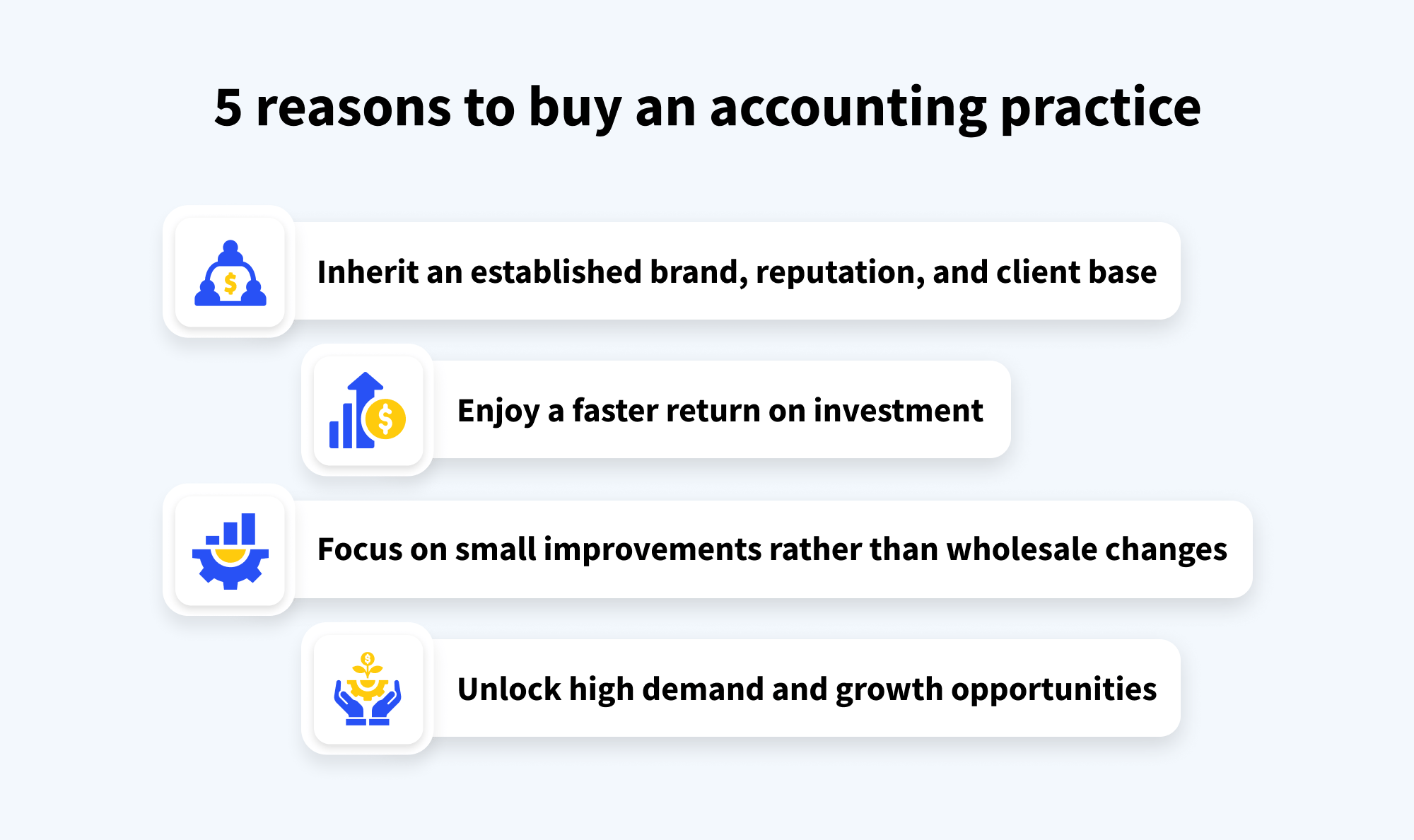

Why buy an accounting practice?

If you want to become the owner of an accounting practice, you have two options: start your own or buy an existing business. While acquiring an accounting practice involves a greater initial investment, there are plenty of reasons why it’s an attractive proposition. Let’s explore some of the key advantages.

All the benefits of an established practice

When you start your own accounting firm, it takes a while to build a client base and reputation. Acquiring an existing business means those foundations are already laid. You get to own a business with real momentum, a loyal client base, and steady revenue. You’ll already have an established brand and reputation. If the firm is big enough, you’ll have a ready-made team of professionals who know the firm’s processes and clients inside out.

That’s exactly what Andrea MacDonald was aiming for when she started looking. But the unexpected value came from how the acquired team worked.

Faster return on investment

Buying a practice represents a major investment, but if the business is healthy, you’ll enjoy returns straight away. Acquiring a business is also less risky than starting a new one. Assuming you’ve done your due diligence and the business is financially sound, there’s less risk of it going bankrupt. As a result, you are more likely to be able to secure financing.

Focus on small improvements rather than wholesale changes

Becoming the owner of an established business is an interesting challenge. You can look at existing processes, technologies, and services with a discerning eye and make adjustments and improvements where necessary. Contrast that with starting your own business, where you need to figure out everything from scratch.

High demand and growth opportunities

Now is a great time to become the owner of an accounting practice. With demand for accounting services outstripping supply, you’ll be well-positioned to grow your business. At the same time, modern accounting tech can streamline and automate entire accounting workflows, enabling you to serve a growing client base without having to scale your team.

Expand an existing accounting business

If you already own an accounting practice and business is booming, acquiring another business can be an excellent way to extend your reach and expand your client base. While incorporating a newly bought business into an existing one can be a sensitive process for employees and clients alike, the potential benefits are huge.

Types of accounting practices to consider

No two accounting practices are the same, so an understanding of the pros and cons of different options is crucial. Here, we’ll focus on some important factors to weigh up on your journey to becoming a business owner.

What type of accounting practice do I want to buy?

The first thing to think about is the type of accounting firm you want to acquire.

Andrea’s advice is clear: get specific about what you’re really looking for. And the first step is deciding whether you want to buy a solo practice, a small business, or a large firm.

Let’s look at the characteristics of each.

Solo practices

As the name suggests, solo practices comprise one person — the owner. They may occasionally hire freelance staff to help out with certain business-related tasks, such as website building or content marketing, but they generally handle the accounting work themselves.

Here are some characteristics of solo practices:

- Usually fully remote — i.e. no physical office space

- Provide a more personalized, hands-on approach to client management

- Quick to adopt modern tech, such as cloud platforms, automation tools, and AI

- Focus on specific services, such as tax preparation

- Require hands-on management from the owner

- Relatively young in business terms

Small businesses

While there’s no official definition of a small accounting practice, businesses in this category typically have a team of between 2 and 10 employees. Like solo practices, they are often fully remote, but some may have a high-street presence with a small office.

Small businesses tend to drive more revenue than solo practices, but there are also likely to be higher overheads, with multiple software licenses, office equipment, and staff salaries to cover. They’ll usually offer a broader range of services than a solo practice.

Medium-sized and large firms

In this category, accounting firms have large teams, which may be spread across multiple office locations. In addition to accountants, they’ll have in-house staff covering areas such as IT and marketing — or they’ll outsource these functions to third-party services.

Here are some characteristics of medium-sized and large firms:

- Serve large client bases consisting of established business clients

- Have a strong brand and reputation

- Less agile and slower to adopt new technology and best practices

- Offer a broader range of accounting services — and charge higher fees

- Much more expensive to purchase, with high overheads

General vs specialized services

In most cases, larger firms offer broader services than small firms. That said, firms of any size may choose to specialize in specific areas of accounting, or target certain industries or client segments over others.

For example, some firms focus solely on tax preparation, while others specialize in audit or consulting. Some might tailor their services to tech startups, while others focus on the healthcare industry, or hospitality, or any other niche. Then there are firms that offer pretty much every type of accounting service to any type of client.

There are pros and cons to different approaches. Accounting firms that offer general services can cast their nets wider, but they may struggle to stand out from the crowd. Those that specialize in niche areas of the industry have the opportunity to corner the market but are targeting a much smaller cohort of clients.

With so many different types of firms to consider, the best opportunities will depend on factors such as your goals, preferences, and personal accounting experience and expertise.

Geographic considerations

For traditional brick-and-mortar businesses, location is another key factor to consider when looking to buy an accounting practice. An accounting practice’s location can affect the type of clients it might serve, the competition it faces, and its potential for growth.

Practices in large, busy cities will face stiffer competition, but they also have access to a larger target market and can generally charge higher fees. Practices in smaller towns or more rural areas typically have less competition and more loyal client bases.

Of course, many smaller firms today choose to be fully remote. This brings huge benefits, including lower overheads and the potential to attract clients from across the country. On the flip side, however, more traditional customers may prefer a local business with a high-street presence, making it more challenging for remote firms to establish themselves.

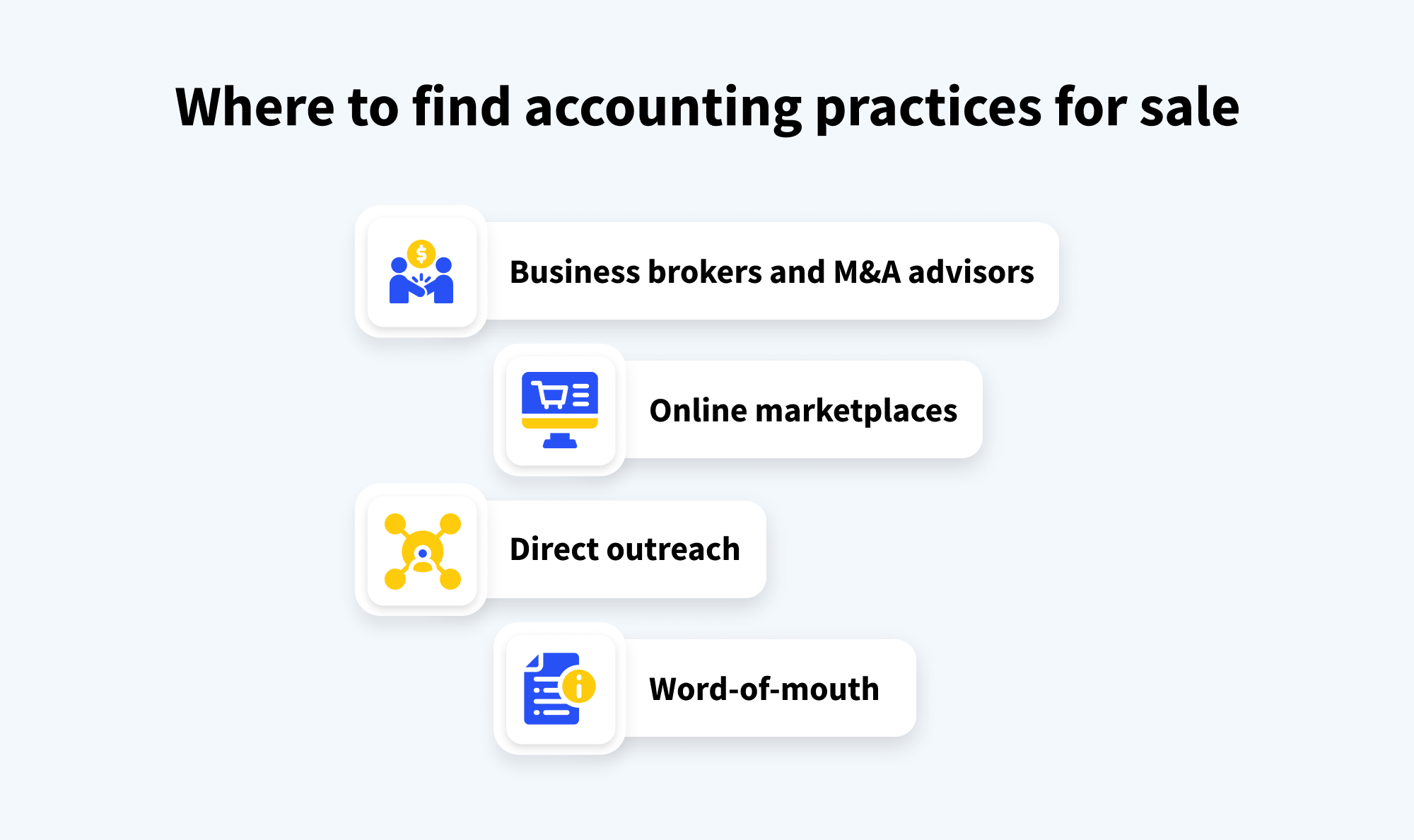

Where to find accounting practices for sale

Now you know the type of accounting practice you’d like to buy, it’s time to start your search. There are several avenues you can explore to find the perfect opportunity. In this section, we’ll shine a light on the most effective ways to find accounting practices for sale.

Business brokers and M&A advisors

Business brokers help to connect those looking to buy a business with those looking to sell. For a cut of the fee, they’ll guide you through the purchase process. There are plenty of general brokers out there, but you might want to consider those that specialize in accounting and tax practices. For example:

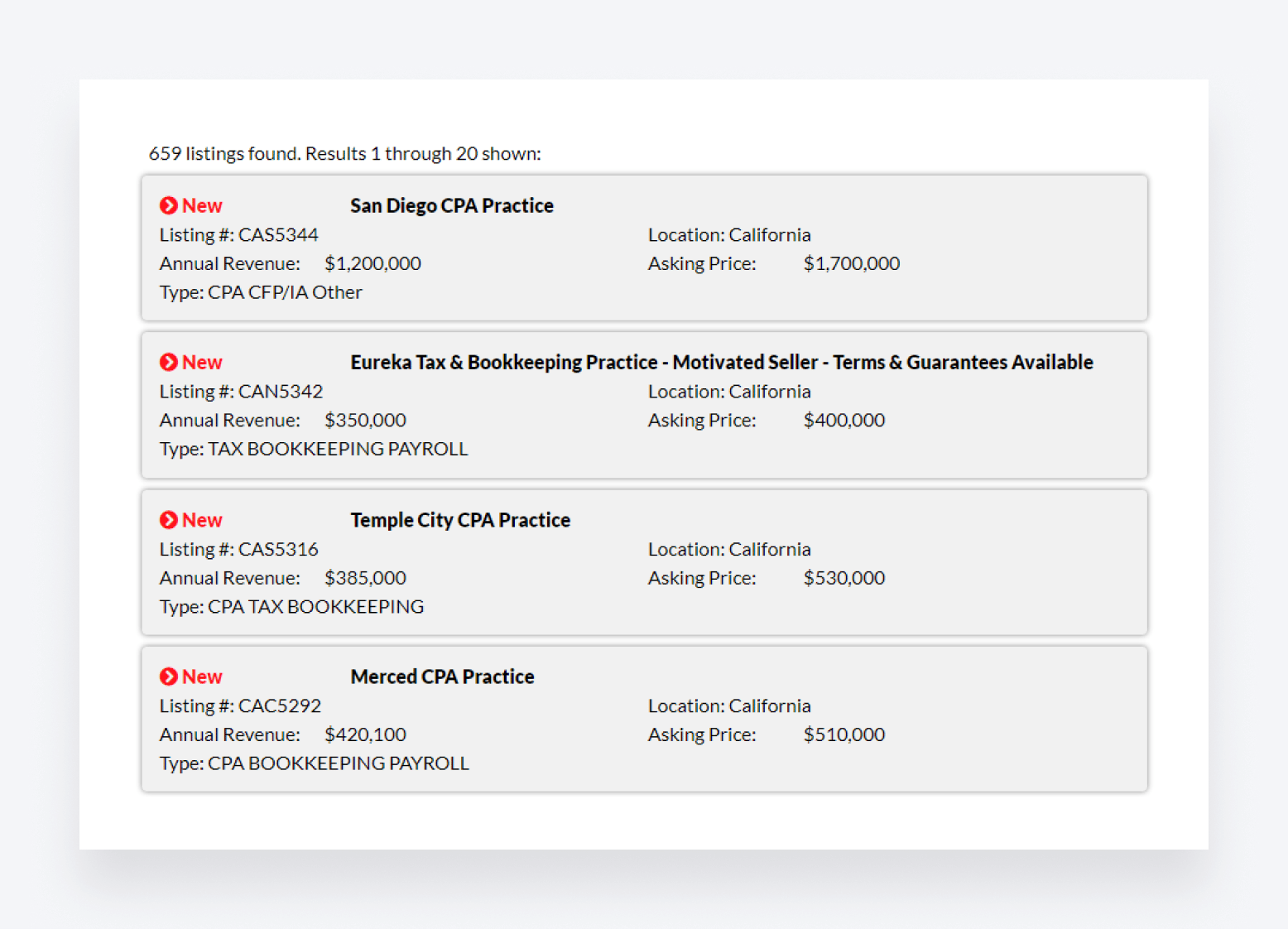

Brokers typically list businesses for sale on their websites, although they may also have access to listings that aren’t advertised publicly. A quick search on Accounting Practice Sales’ website for listings in California brings up over 650 results! As you can see, the listings show not only the price but also the annual revenue.

Like business brokers, mergers and acquisitions (M&A) advisors help facilitate the process of buying a business. Where they differ is the scope of their services and, in many cases, the size of the businesses in question.

Where business brokers might focus on the sale of smaller, local businesses, M&A advisors might facilitate the sale of larger companies, often involving more complex legal transactions, including mergers, restructuring, bankruptcy and insolvency, capital advisory, and more. Generally, M&A advisors will offer a broad range of services, including market assessment, due diligence, and earnings analysis.

Online marketplaces

Online marketplaces are another great way to find accounting practices for sale. Like business brokers, these platforms list businesses across various industries, including accounting firms, and allow you to search by location, size, and price. Unlike brokers, however, they don’t facilitate the actual transaction. Here are some examples:

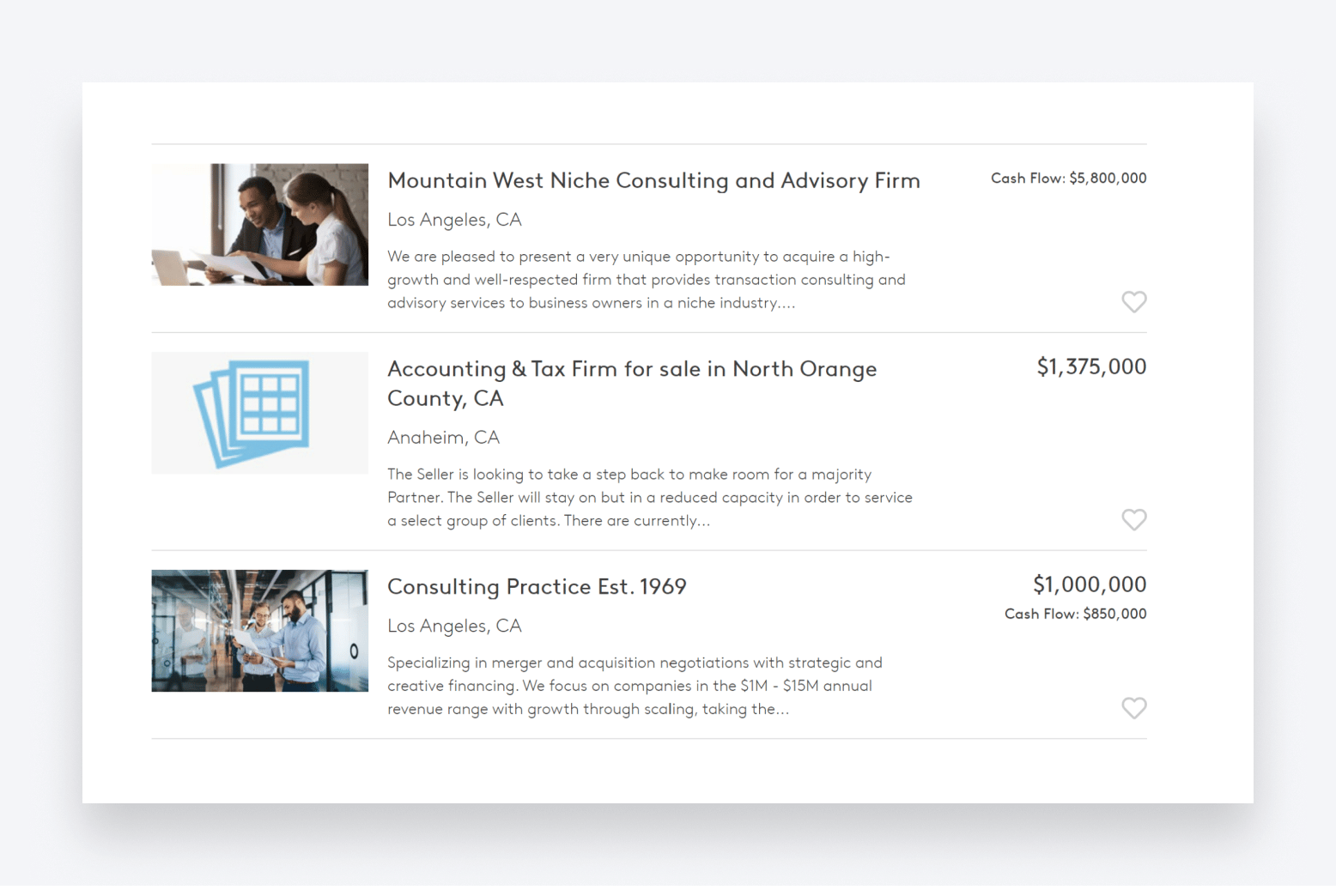

Here are some examples from BizBuySell, showing listings for financial services businesses in California:

Direct outreach

One of the simplest ways to find potential accounting practices for sale is to keep your eyes open. If you see a business you like the look of, whether online or “in real life”, you could consider contacting them directly to inquire. Of course, this approach must be handled very sensitively to be successful — business owners won’t want to sell to anyone they perceive to be stong-arming them.

Word-of-mouth

Another approach is good old-fashioned word of mouth. Sometimes, the best opportunities are found by getting out there into the accounting community, asking around, and keeping your ears to the ground. Here are some ways you can do this:

- Develop a strong network of accounting peers

- Join accounting groups on LinkedIn or Slack

- Attend industry events and conferences to meet new people

- Maintain memberships with professional accounting bodies, such as AICPA

What to consider before purchasing an accounting firm

Before you purchase a new accounting business, you need to conduct thorough research and due diligence. The work you put in at this early stage could be the difference between success and failure. Here are some factors to consider before you make your move.

Assessing the practice’s financial health

Financial due diligence is crucial to understanding whether an accounting business represents a good opportunity or not. Make sure you examine the business’s financial statements to assess how profitable and financially stable it is.

You should also look at revenue trends, profit margins, and cash flow over the past few years. Ideally, you want the business to show consistent earnings over that time. Any significant fluctuations could indicate underlying issues.

Additionally, pay close attention to the practice’s debts and outstanding liabilities. You want to make sure the business is on sound financial footing, not encumbered with debt that could hamstring its profitability going forward.

Evaluating its client base and retention rates

An accounting firm’s client base is one of its most important assets. It’s what drives revenue and keeps the lights on, after all. During your due diligence, take time to analyze the firm’s client base and ask important questions such as:

- Are they primarily small businesses, individuals, or larger corporations?

- What is the proportion of new clients to old ones?

- How many clients pay for recurring services, such as payroll, financial reporting, or tax filing?

- Is revenue spread evenly across clients, or does a small proportion of clients provide a majority of income?

- What are the client retention and attrition rates?

The answers to these questions will teach you a lot about the business. For example, a large proportion of older clients will show that clients are generally happy and loyal, but that increased efforts could be made to acquire new clients. High attrition rates are a clear indicator that something isn’t right.

Understanding staff and operational dynamics

Alongside clients, a business’s most important asset is its employees. The stronger and more stable the team, the more successful the practice is likely to be. At this point, it’s a good idea to look into the experience, expertise, and tenure of the practice’s staff. If it’s a larger business, an organization chart is a useful way to understand the organizational structure, reporting chains, and levels of seniority.

You’ll also need to understand how the business works from an operational standpoint. Pay close attention to the firm’s tech stack and how efficient internal workflows are.

Undertaking legal and regulatory compliance checks

Besides evaluating the practice’s finances and operations, you’ll need to ensure that it complies with all relevant legal and regulatory requirements. This involves checking that the business:

- Has all proper licenses up to date

- Adheres to industry standards

- Is compliant with the latest tax and employment laws

When it comes to compliance, it’s also worth looking at the practice’s history. Has the business ever been the subject of any controversies, lawsuits, or fines? If so, what caused them, and how were they resolved? Ideally, you want to acquire a business with no reputational or legal baggage.

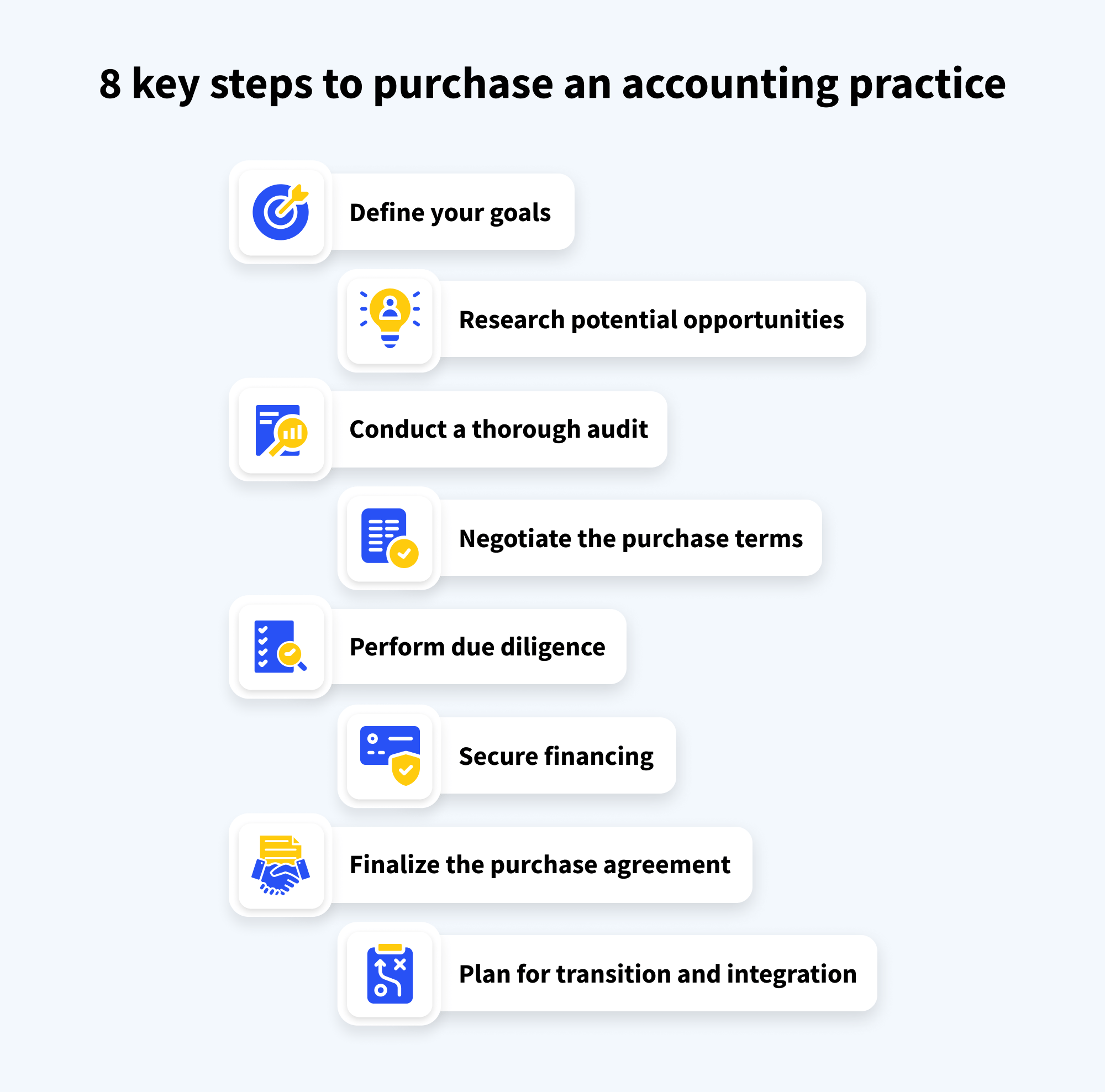

8 key steps to purchase an accounting practice

There’s so much to consider when purchasing an accounting business. To ensure you don’t miss something important, let’s break the process down into some key steps.

1. Define your goals

When making a major professional decision, it often helps to start with the why. Why bother going through what can be a complicated process in the first place? What are you hoping to achieve? By clarifying your objectives at this early stage, you’ll have a better understanding of the type of practice you want to buy.

When defining goals, it’s a good idea to be as specific as possible. Set clear criteria for what you’re looking for — from the size and location of the business to financial targets, client-base profiles, and daily operations.

2. Research potential opportunities

Once you’ve defined what you want to achieve by acquiring an accounting practice, you can start searching for ones that align with your criteria. As we covered earlier, you can peruse online listings or tap into your accounting network to find opportunities that fit.

Once you’ve honed in on a business, you can engage a business broker or M&A advisory firm to facilitate the purchase process.

3. Conduct a thorough audit

Before moving forward with any opportunity, you’ll need to conduct a comprehensive audit of the practice. This will help you get a clear picture of the practice’s situation from both a financial and operational standpoint. Here are some steps you can follow:

- Review the business’s financial statements, revenue trends, profit margins, and debt levels

- Assess its tech infrastructure, including accounting software, data management systems, and cybersecurity measures

- Analyze its client list, focusing on retention and attrition rates

- Evaluate the skills, experience, and stability of the current team

- For larger firms, familiarize yourself with the organization structure and reporting chains

- Look at online reviews to understand client satisfaction

4. Negotiate the purchase terms

If everything in stage three checks out, it’s time to make your move and enter into negotiations with the seller. Generally, accounting practices that are listed for sale will have a suggested asking price, but this is often negotiable.

If you feel like the suggested asking price is too high, you could engage a firm that specializes in business valuations. There are multiple ways to value a business — for example based on a multiple of financial data such as earnings or assets, or by looking at how much similar businesses were sold for. Once you’ve come to a number you think is fair, you can make your opening offer.

Besides price, be prepared to negotiate aspects such as transition periods, the retention of staff, and non-compete clauses. Given the complexity of these negotiations, we recommend working with legal professionals to ensure an agreement that is both fair and beneficial.

5. Perform due diligence

If your offer is accepted, you’ll need to conduct a detailed due diligence process before finalizing the deal. This typically involves checking all the information provided by the seller, including legal and regulatory compliance and any outstanding liabilities.

Essentially, conducting due diligence will help ensure that there aren’t any financial or legal skeletons hiding in the closet. Again, because of the importance and potential complexity of this process, we recommend working with legal professionals who specialize in due diligence for commercial acquisitions.

6. Secure financing

If you’re paying for the practice in full with cash, you can skip this step. If not, you’ll need to secure financing. There are several options available when it comes to financing a business purchase, each with its own pros and cons. For example:

- Traditional bank loans — these often offer the most competitive rates but can be difficult to qualify for

- Small Business Administration (SBA) loans – provided by government-approved lenders, these loans are typically easier to qualify for than traditional bank loans

- Seller financing — instead of getting a loan, you can strike an agreement with the seller whereby they provide you with credit for the purchase

- Partnerships — by entering into a partnership, you can pool your financial resources with other partners, who will hold joint ownership and responsibility for the business

- External investment — outside investors can provide you with funds, often in exchange for equity in the business and a role in decision-making

7. Finalize the purchase agreement

If both parties are happy that all conditions are met, you can finalize the purchase agreement. A purchase agreement is a legal document that outlines the terms of the sale, including the price, payment structure, and any warranties or representations. We recommend working closely with a lawyer to ensure that everything checks out.

8. Plan for transition and integration

Once the purchase has been completed, it’s time to focus on transitioning ownership and integrating the practice into your operations. The smoother this process, the better — especially for staff and clients. Make sure you communicate clearly with all parties involved and try to ensure as much continuity in services and workplace practices as possible.

That’s why your first job post-acquisition is to bring consistency. Standardize how the team works, communicates, and accesses tools. For Andrea, that started with something as simple — and essential — as issuing company-owned laptops and tightening IT security. It’s a signal: we’re one firm now, and we’re doing things right.

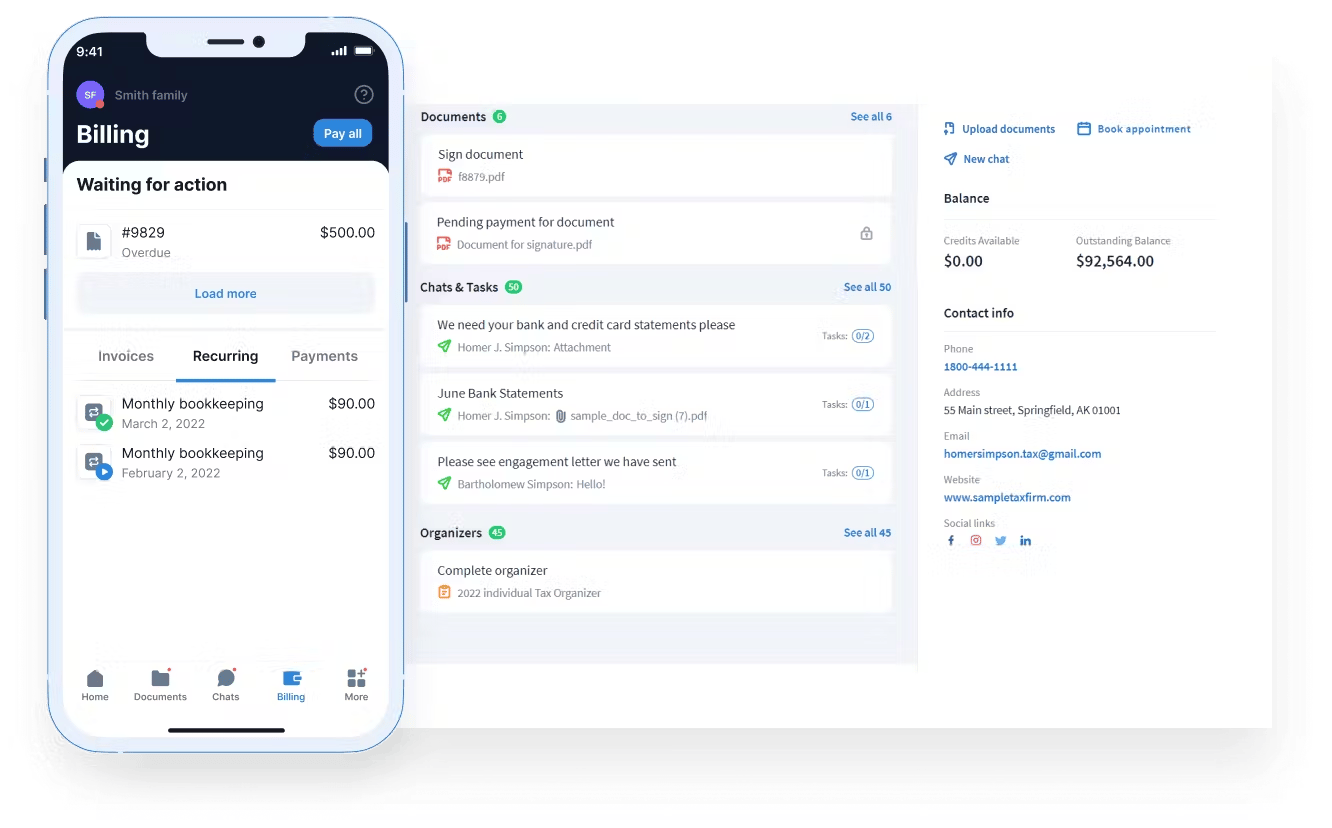

Choosing the right technology will help you organize and streamline your operations from day one. With TaxDome, you can use customizable templates to implement automated workflows and accounting best practices rapidly. This means less time battling with administrative tasks and more time focusing on making your new practice a success.

Potential challenges and how to overcome them

Buying an accounting business can be fraught with challenges. In this section, we’ll highlight some of the key issues you may encounter — and how to avoid them.

Overpaying for the practice

It’s easy to assume that the asking price for a business reflects its true value, but in some cases, business owners may set the price higher to see who bites. Other times, multiple interested parties may drive the price up way beyond the asking price, meaning whoever wins the bidding war is almost certainly overpaying.

To avoid these issues, conduct a thorough valuation using tried-and-tested multiples methods — e.g. asset-based, income-based, or market value. We recommend using an external valuation expert to help with this process.

Underestimating financial needs

Even with a fair price, the real costs often come after the deal closes. Strong projections don’t always hold up in practice. Between onboarding costs, tech upgrades, and shifts in staffing, the financial runway you planned for might not stretch as far as expected.

Andrea’s guidance here is straightforward:

The takeaway? Building a healthy buffer early on can be the difference between a confident transition and a cash crunch.

Client retention issues

Andrea’s point is an important one, and those feelings can quickly turn into a bigger risk. Once the acquisition is complete, you may experience some issues with client retention — especially if it’s a small business and clients were on good terms with the previous owner. To make this kind of reaction less likely, you can:

- Maintain open communication — tell clients who you are and outline your commitment to providing an outstanding service to them

- Retain key members of staff that clients may be familiar with and trust

- Ensure continuity in the services you offer and their quality

- Ask the previous owner to endorse your ownership and explain to clients that they are in good hands

One of the best ways to ensure your clients stick around is by delivering an incredible client experience — and that means choosing the right technology. With a practice management platform like TaxDome, your clients can manage all of their touchpoints with your firm via a secure client portal, available on either desktop or our top-rated client mobile app.

Resistance to change

You may have clear ideas about how you want your business to be run, the technology you want to use, or the direction you want to take going forward. If these ideas clash with the business’s existing processes and culture, you may find that existing staff are resistant to change.

Andrea experienced this firsthand when she bought a firm:

Again, the key here is clear communication. You can build bridges by asking staff which processes they think work and which could be improved. If you plan to make major changes, you should clearly articulate why and what benefits they will bring.

Hidden liabilities

In some cases, the business you acquire may have undisclosed liabilities, such as legal issues, outstanding debts, or compliance problems. You might only discover these after the purchase, leading to unexpected costs and other issues.

The only way to avoid hidden issues is to conduct a thorough due diligence process, ideally led by an experienced legal professional. You could also consider purchasing representations and warranties insurance to protect you against such undisclosed liabilities.

Staff turnover

As we touched on earlier, you may find that staff are unsettled by the acquisition. In some cases, key team members may choose to leave, leading to a loss of expertise, damaged client relationships, and operational issues.

The best way to avoid post-acquisition turnover is to engage with staff early and address any concerns they may have. Get to know them on a personal level. You could even offer staff incentives for staying, such as retention bonuses or career development opportunities. Ultimately, it’s all about building trust.

To sum up

Acquiring an accounting practice can be a transformative move in your professional career. Instead of starting a business from scratch and all the uncertainties that go with it, you get to inherit a practice with an established brand, reputation, team, and client base.

Yet while there are clear benefits to purchasing an accounting practice, there are also plenty of potential challenges and issues to overcome. The good news is you can overcome those challenges with careful planning, support from legal professionals, and a good deal of patience.

We hope you’ve found the information in this article helpful. Keep these insights on hand — download our practical guide to buying an accounting firm, complete with actionable steps and Andrea MacDonald’s expert tips.

Whether you’re leading an accounting team or looking to buy an accounting practice, the best way to achieve greater efficiency and results is with the right tech. With TaxDome, you get all the tools you need to manage your firm, team, clients, and processes, all on one easy-to-use practice management platform.

TaxDome became Andrea’s firm-wide hub — not just for managing clients, but for visibility into every moving piece of the business.

To see how TaxDome can help you take your accounting practice to the next level, request a demo today.

Josef creates clear, actionable content at TaxDome, highlighting features, updates, and key accounting topics. His focus is on making complex ideas accessible and engaging, helping users understand and apply insights effectively.

Get your free guide

Thank you!

The guide copy has been sent to your email. Please check your inbox!

Recommended articles

Proven strategies to grow your accounting firm with a downloadable guide inside

ChatGPT for accountants: 12 strategies to automate your workflows

How to start an accounting firm: a step-by-step guide to running your own practice