The accounting cycle is a process of recording and reporting a company’s financial transactions.

Usually, it consists of eight steps that are repeated during each reporting period. The accounting cycle ensures that financial data is accurately stored and presented. The process begins when the transaction occurs and ends when it’s included in the financial statement.

The accounting cycle helps businesses maintain an organized approach to financial reporting, which is essential for decision-making and regulatory compliance.

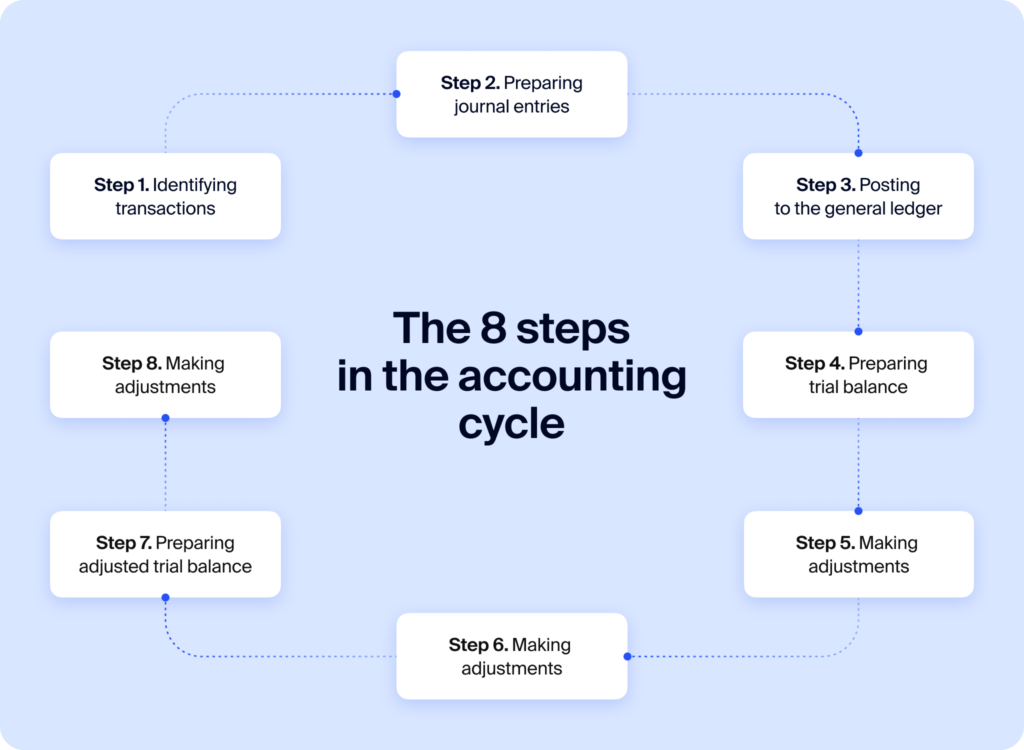

The accounting cycle includes the following steps:

- Identify transactions: note down any business event or transaction that affects the company’s finances, like sales, purchases, or payments

- Make journal entries: write each transaction in a journal, using the double-entry bookkeeping method

- Post to the ledger: transfer the journal entries to the appropriate accounts in the general ledger

- Prepare trial balance: list out all the account balances to check if the total debits equal the total credits

- Make adjustments: if there are any discrepancies in the trial balance, make necessary adjustments for accruals, deferrals, and estimates

- Prepare an adjusted trial balance: after incorporating adjustment entries, prepare an adjusted trial balance

- Prepare financial statements: use the adjusted accounts to prepare such financial reports as the income statement, balance sheet, and cash flow statement

- Closing entries: transfer temporary account balances to permanent accounts and prepare the accounting records for the next accounting period

The company often does post-closing trial balance to verify the equality of debits and credits after closing entries.

The accounting cycle is a continuous process that may be repeated monthly, quarterly, or annually. Companies follow this process to ensure accurate and timely financial reporting, which helps maintain financial records and assess performance.

Frequently asked questions

Why is the accounting cycle important?

The accounting cycle is important because it helps businesses with:

- Keeping accurate financial records

- Understanding their financial performance

- Making well-informed decisions

- Following laws and tax regulations

- Promote transparency and accountability in record-keeping

Is an accounting cycle different from an operating cycle?

Yes, these are two different concepts.

The accounting cycle focuses on the process of recording and reporting financial transactions, while the operating cycle refers to the events involved in converting resources into cash through the production and sale of goods or services.

Is an accounting cycle different from a budget cycle?

Yes, these are two separate yet interrelated processes.

The accounting cycle involves recording and reporting actual financial transactions that have occurred during a specific period, while the budget cycle refers to the process of planning, preparing, and monitoring a company’s budget, which is an estimate of future revenue and expenses.

Who is responsible for performing the accounting cycle?

The accounting cycle is typically performed by accountants, bookkeepers, or finance professionals. The specific roles and responsibilities may vary depending on the size and structure of the company.