Debit and credit are fundamental concepts in double-entry accounting that represent the two opposite aspects of financial transactions.

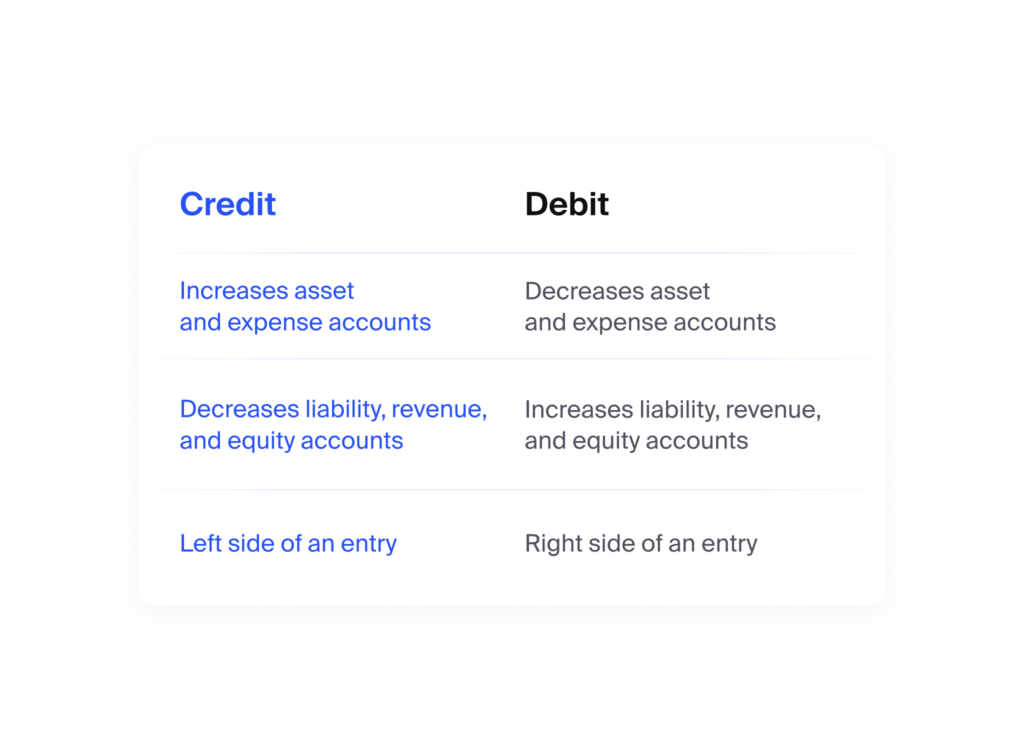

A debit is an increase in an asset or expense account, or a liability or equity account.

A credit is a decrease in an asset or expense account, or a liability or equity account.

In other words, debit and credit entries are used to record increases or decreases in various accounts, ensuring that this fundamental accounting equation remains balanced:

In double-entry accounting, every transaction involves at least one debit entry and one credit entry of equal value, ensuring that the total debits and credits remain equal.

Frequently asked questions

How do you determine whether to debit or credit an account?

Generally, asset and expense accounts are debited for increases and credited for decreases. The liability, equity, and revenue accounts are credited for increases and debited for decreases.

Can a debit have a negative value or a credit have a positive value?

Yes, it is possible for a debit to have a negative value or a credit to have a positive value, depending on the context of the transaction.

For example, negative debits and positive credits are used when adjusting entries, reversing entries, or reflecting contra accounts.