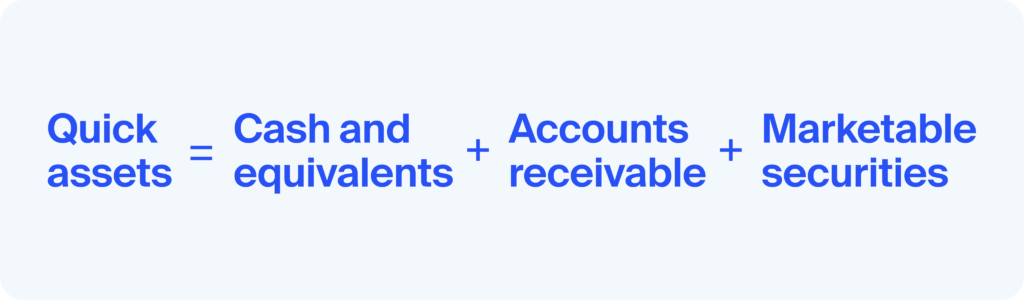

Quick assets are calculated by adding together cash and cash equivalents, accounts receivable, and marketable securities:

Before calculating quick assets, you first need to analyze financial statements to identify them on a company’s balance sheet:

- Cash and cash equivalents: look for line items like “Cash,” “Petty cash,” or “Cash at bank.” Cash equivalents include short-term, highly liquid investments and could be mentioned as “Short-term investments”.

- Marketable securities: short-term, easily tradable investment securities like stocks and bonds that can be quickly sold on a stock exchange.

- Accounts receivable, usually listed as “Accounts receivable” or “Trade debtors.” However, you’ll need to consider the collectibility of these receivables by using aged receivable reports to assess the likelihood of collecting them.

Frequently asked questions

Can inventory be considered quick assets?

Inventory is generally not considered a quick asset because it takes time and effort to convert it into cash.

Can prepaid expenses be considered quick assets?

Prepaid expenses typically don’t qualify as quick assets due to their less immediate liquidity.

Prepaid expenses such as rent or insurance paid in advance technically represent a future benefit rather than a directly convertible asset.