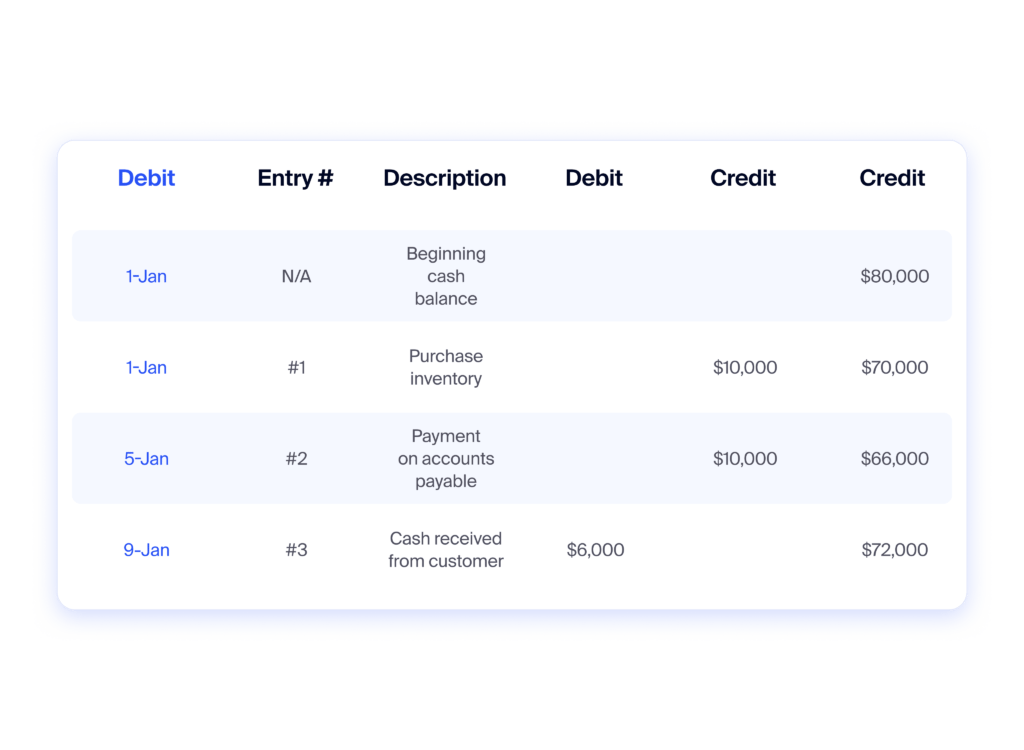

A ledger, or general ledger, is a central record-keeping book for all financial transactions of a business or organization.

It provides a comprehensive view of all account balances and transactions over a specific period of time.

The primary functions of a ledger are:

- Recording transactions from various accounting journals and systematically posting to the respective accounts in the ledger

- Maintaining balances of each account by recording debits and credits based on the double-entry accounting system

- Facilitating financial reporting by using information recorded in the ledger to prepare financial statements, such as the income statement, balance sheet, and cash flow statement

There are different types of ledgers commonly used in accounting, these include:

- General ledger: the primary ledger that contains all the asset, liability, equity, revenue, and expense accounts of a business. It serves as the central repository for all financial data

- Subsidiary ledgers: secondary ledgers that provide more detailed information about specific accounts from the general ledger, e.g. accounts receivable ledger or accounts payable ledger

- Private ledger: a ledger that is used to record personal or confidential financial information that is kept separate from other accounting records

Frequently asked questions

What is the difference between a ledger and a journal?

A ledger is a collection of accounts that summarizes and organizes the transactions from the various journals.

A journal is the initial record where financial transactions are recorded in chronological order as they occur.

While journals provide a chronological record of transactions, ledgers provide a comprehensive view of account balances.

Can ledgers be computerized or automated?

Yes, modern accounting software often includes automated ledgers.

Instead of manually posting transactions to individual accounts, the process can be automated based on predefined rules and settings.

Transactions are automatically recorded and updated in the respective accounts within the digital ledger, increasing efficiency and reducing the risk of errors. However, human oversight and review are still necessary to ensure the accuracy of the ledger entries.